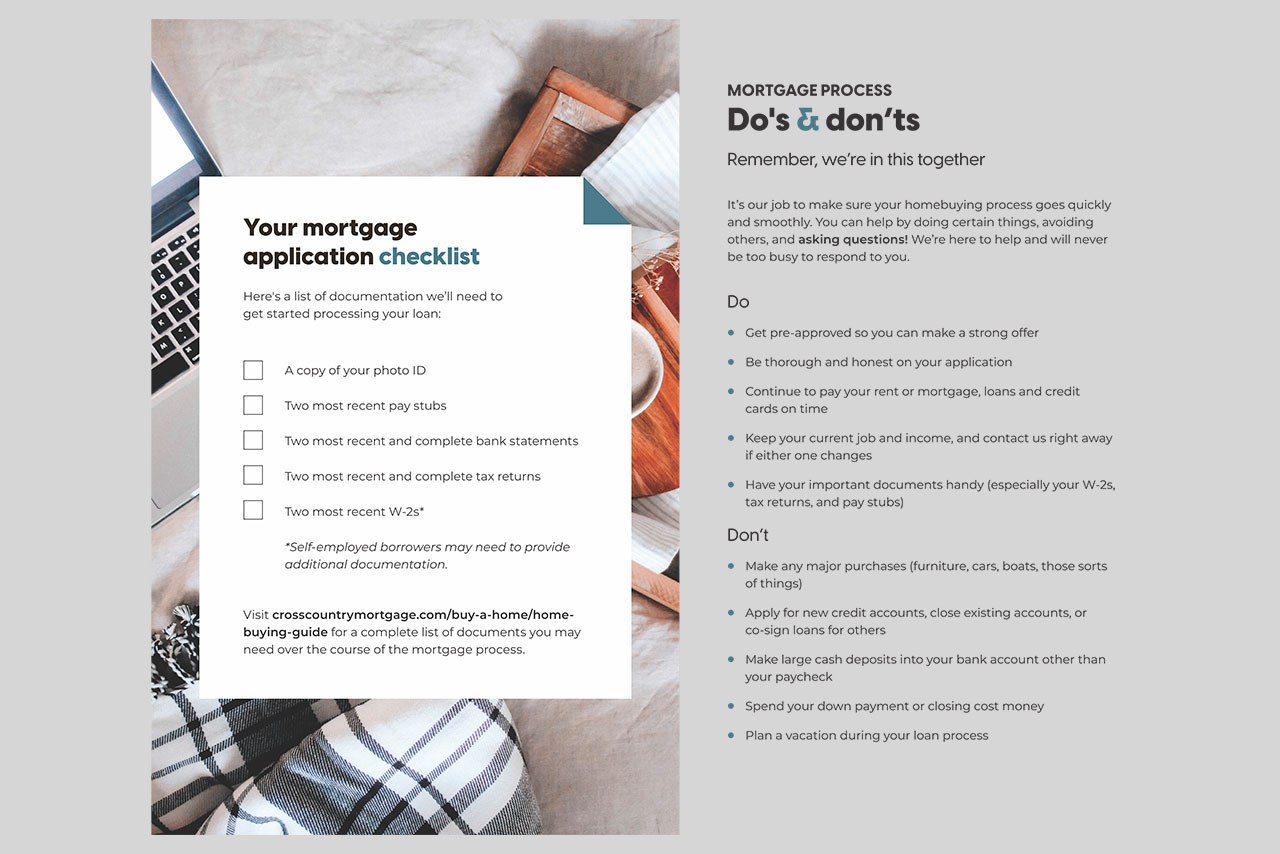

Refinancing Guide: Steps to Refinance a Mortgage

Whether you want a lower monthly mortgage, a shorter term, or a fixed interest rate, refinancing your mortgage can help. We’ve outlined the steps involved, from start to finish, to make sure you have a smooth and successful experience.

F. A. Q's

7 steps to refinance your mortgage

Here are the seven steps to refinance your house. You’ll also find these in the downloadable Refinance Guide

Your credit score is not the only factor in getting approved for a mortgage refinance, but it’s an important part of determining what you’ll be able to qualify for.

Check your own credit score – and make sure it’s accurate – before meeting with a lender. You can get a free credit report once a year online by visiting annualcreditreport.com.

- Verify the report for accurate information

- Report and dispute inaccuracies with the credit bureau (disputes in process may delay loan approval)

- Paying down high credit balances may positively affect your credit score

- By paying down applicable lines of credit before applying for a loan, you may qualify for getting approved for a better interest rate

Set up payment plans

Call your creditors and work out a budget-friendly payment plan on delinquent accounts prior to applying for a loan. Work out a plan that won’t harshly affect your debt-to-income ratio but will still let lenders know you’re serious about being accountable for your debts.

Start with a free loan officer consultation. We’ll help you decide if refinancing makes sense for your specific financial situation and match you with the right refinance loan product.

It’s time to start the loan process. Meet with your licensed loan officer to help you gather paperwork and submit your mortgage application.

Gather all the required identification and paperwork

Some refinance loan products, like FHA Streamline Refinance Loans or VA Interest Rate Reduction Refinance Loans (VA IRRRL), may not require all of this paperwork. And in other cases, this list may not be all-inclusive, but you may be able to expedite the process by having these documents on hand.

Identity and income information

- Your full legal name, Social Security number, and date of birth, plus a copy of your Social Security card, which may be required

- Your phone number, email address, and residential mailing addresses for the past two years

- Your primary and secondary income and sources

- Your government-issued photo ID

- All employer names, addresses, and phone numbers for the past two years

- The values of your bank, investment, and retirement accounts, as well as any other asset accounts

- Your monthly debt obligations

- The address of the mortgaged property, year built, estimated home equity amount, and home value

- History of annual property taxes, homeowners insurance, and homeowner association dues (if any)

Income information for self-employed borrowers

- Your personal and business federal tax returns for the past three years

- A year-to-date profit and loss statement

- Documentation to show your business has made 12 consecutive monthly payments on any personal debt in your name

Credit information

- A letter of explanation for any late payments, judgments, collections, or other derogatory credit history items

- Source of funds documentation for any large deposits on asset or bank statements

- The judicial decree or court order of each obligation due to legal action

- Bankruptcy/discharge papers for all bankruptcies in your credit history

Income and tax documentation

- IRS Form 4506-T (we will provide this form)

- Your W-2s for the past two years

- Pay stubs for the past 30 days

- Your federal tax returns (1040s) for the past two years

- Most recent quarterly or most recent two months’ asset and bank statements for all accounts on your application (all pages, including blank pages)

- Homeowners insurance information, including the agent’s name and phone number

Fill out and sign the loan application — including the fair lending notice, loan info sheet, and credit authorization.

Review your loan estimate

This document contains important details about the loan you’re applying for, including estimations of your interest rate, monthly payment, closing costs, taxes, insurance, and any prepayment penalties. The lender must provide this document to you within three business days of receiving your application.

Clear any additional requests from underwriting

Underwriting is the department that reviews all your identification, income and asset documentation, and credit history to assess if you will qualify for the desired loan. They determine the terms of the loan and will occasionally require extra documents to fully understand your background to make their decision. It’s important to make yourself available during the underwriting process and to respond to any requests promptly and thoroughly.

Consider the home appraisal

When refinancing your house, not everyone is required to get a home appraisal. However, it could be in your best interest to get a home appraisal for your refinance because the risk is the lender doesn’t assign a high enough value to your home, thereby restricting the type of mortgage loan products that may be available to you. An accurate appraisal will prevent the lender from basing the refinance loan on too small of a home value.

Make sure the amount, payments, rate lock, and other details are clearly stated in writing in a signed document.

Closing on your mortgage refinance usually takes place in the presence of a public notary, and if you have a co-applicant, then they will also need to be present.

You should be prepared for several things:

- Review the final documents and make sure the rates and amounts are what you’ve agreed to

- Bring a cashier’s check to cover the closing costs and down payment – personal checks are usually not accepted

- Sign the loan and be prepared to show photo ID and possibly a Social Security card

The lender must provide this document to you at least three business days before you close your loan. This document contains the final terms of your loan. Use this time frame to review it thoroughly and compare it to your Loan Estimate document. Don’t be afraid to ask your lender questions if you are unclear about the terms.

What’s next?

Congratulations, you can cross “refinancing” off your to-do list, but more importantly, you’ve either uncovered ways to save or ways to more easily manage the expenses that life has in store for you. Either way, the financial benefits are well worth the effort.

We’re here to offer you guidance on any future questions or situations that may arise with your loan. A licensed loan officer will always be available to help you refinance, use your home equity, or even purchase additional properties to build your investment portfolio.